KYC Compliance Requirements: Your Top 10 Questions, Answered

It's critical for fraud pros at financial institutions to stay on top of KYC compliance requirements in order to maintain regulatory adherence and keep bad actors out of their system. Here are the top 10 things you need to know about KYC. Whether you're looking to refine your compliance strategy or clarify specific requirements, this post has you covered. Let's dive in!

1. What does KYC stand for?

KYC is an acronym for Know Your Customer. In some instances, financial institutions (FIs) that serve corporate customers consider KYC an acronym for Know Your Client. Don’t let this confuse you! ‘Customer’ and ‘Client’ are used interchangeably when it comes to KYC.

2. What is KYC?

KYC is a federal regulation aimed at reducing financial crime—from bank fraud to money laundering to terrorism funding.

KYC mandates that FIs verify each consumer’s identity and assess the individual’s fraud risk prior to commencing a new customer relationship.

In short, KYC requires institutions to answer two critical questions about their potential customers:

- Is the individual who they claim to be?

- What is the likelihood that the individual will commit fraud or other financial crimes?

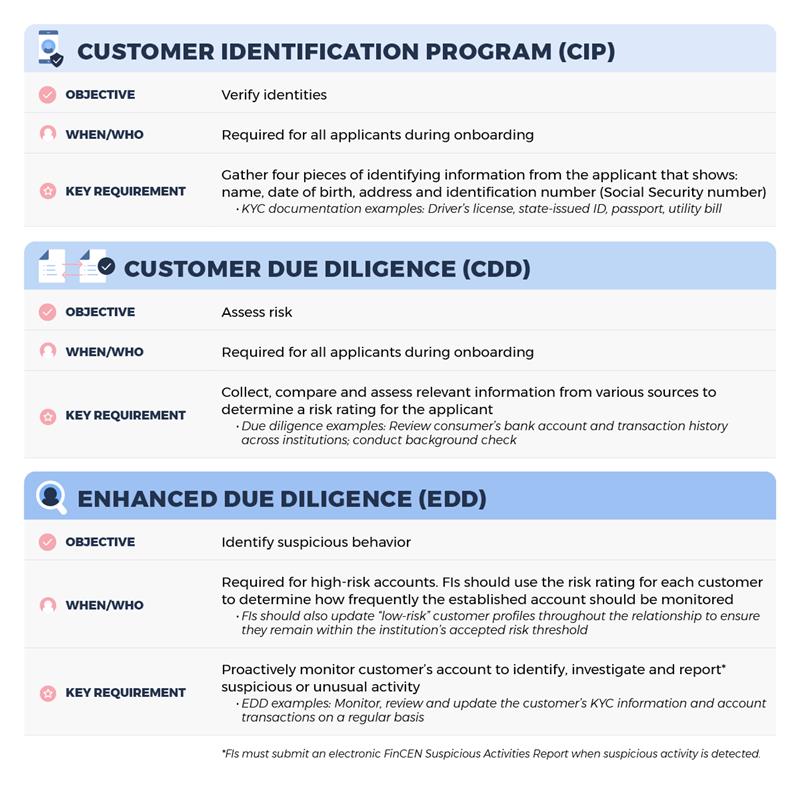

3. What are the elements of KYC—and when are they required?

The two main elements of KYC are the Customer Identification Program (CIP) and Customer Due Diligence (CDD). These two programs work together during account openings to ensure that FIs have a clear view of who they’re dealing with before they onboard any new customers.

A third central element of KYC is Enhanced Due Diligence (EDD). The need for EDD is determined based on the customer’s risk rating.

Let’s look at the details of each.

4. Why do KYC compliance requirements focus mainly on the account opening process?

When bad actors succeed at establishing accounts based on stolen, synthetic or otherwise fraudulent identities, they enjoy a level of anonymity that sets the foundation for fraud. Synthetic identity fraud, in particular, has become a growing concern—with 62 percent of FIs reporting increases in 2024.1

Once a bad actor makes it into the banking system, they have a greater opportunity to commit financial crimes down the road. As such, CIP and CDD are critical first steps for managing fraud risk. By requiring FIs to verify identities and assess risk—at the point of application—these two programs work together to ensure banks do exactly what the regulation spells out: Know your customer.

5. What’s the difference between CDD and EDD?

While CDD is required for all new customers at onboarding, EDD is used to keep tabs on customers who are deemed a high risk for fraud. By continuing to monitor high-risk accounts, FIs can accept more customers—while staying on the alert to proactively identify any unusual patterns of behavior or suspicious activities.

6. What happens if FIs don’t comply with KYC requirements?

FIs that fail to comply with KYC can be hit with significant fines and penalties.

7. What is a Customer Acceptance Policy?

FIs are responsible for developing their own KYC initiatives. They must establish their own standards and policies for complying with the various elements of KYC (CIP, CDD and ongoing monitoring). And that includes developing a Customer Acceptance Policy (CAP), which defines the level of risk the institution is willing to take on when accepting new customers.

8. What is AML and what does it have to do with KYC?

The KYC processes an FI puts in place must adhere to anti-money laundering (AML) standards. As the name implies, AML standards are designed to prevent money laundering—and “knowing your customer” is a critical component of the AML framework.

9. What are common KYC challenges?

- Customer experience: Adhering to KYC processes (e.g. verifying identities and determining a risk rating) can add friction to the account opening process—leading to increased account abandonment and loss of potential revenue.

- Maintaining compliance: Establishing KYC processes and staying compliant can be difficult in the financial landscape—where regulations are constantly evolving.

- Digital shift: As account openings move to digital channels, many FIs are finding it more difficult to authenticate an applicant’s identity and ensure they are who they claim to be.

10. Can banking technology help FIs comply with KYC requirements?

Modern tools are available to help FIs verify identities, assess risk and monitor customer profiles. In 2024, for example, Early Warning® helped banks and credit unions safely open more than 56 million new accounts.

Verify IdentitySM, for example, confirms if a name, DOB and SSN match in real-time to help FIs confidently verify customer identities and assess fraud risk. And because the service works in real-time, FIs can mitigate risk without disrupting the onboarding experience. Simply put, as you gather identity elements from your customers to meet your CIP requirements, you can use Verify IdentitySM to validate the required elements against our National Shared DatabaseSM resource.

Regulatory Compliance: GLBA and KYC Standards

KYC compliance is essential for financial institutions to prevent fraud, money laundering and identity theft. One of the key regulations governing identity verification solutions like Verify Identity is the Gramm-Leach-Billey Act (GLBA).

GLBA mandates that financial institutions protect the privacy and security of consumer data while ensuring that customer identities are verified to prevent fraudulent activity. Under this regulation, institutions must:

- Implement Strong Identity Verification Measures. Financial entities must have procedures in place to authenticate customer identities before granting access to accounts or services.

- Safeguard Consumer Data. GLBA requires institutions to secure customer information and prevent unauthorized access.

- Ensure Compliance with Privacy and Security Rules. Organizations must provide clear disclosures about how customer data is used and establish safeguards to protect sensitive information.

By adhering to GLBA guidelines, Verify IdentitySM helps financial institutions meet regulatory requirements while enhancing security and reducing fraud risks.

To learn more about KYC requirements and best practices for compliance, read our Know Your Customer guide.